We examined recent comments from the Federal Reserve and devised a few scenarios to help our members prepare for what’s next.

The Federal Reserve’s Outlook

The profoundly hawkish shift in tone from the Federal Reserve first appeared in their December 2021 minutes. This was evident- from the following quotes:

“…it may become warranted to increase the federal funds rate sooner or at a faster pace than participants had earlier anticipated.”

“…it could be appropriate to begin to reduce the size of the Federal Reserve’s balance sheet relatively soon after beginning to raise the federal funds rate.”

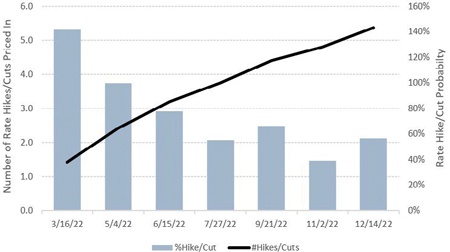

Shortly after the minutes were released the first week of 2022, Bloomberg’s Fed Rate Hike Probability Index moved to a 78% chance for March with a potential three additional hikes by year-end (Exhibit 1). By February, the chances for a March hike reached 100%. Combined with rising bond yields and inflation concerns, there’s no question that the Fed has embarked on the next tightening cycle.

While all signs seem to point to a fast and aggressive Fed tightening, members should avoid predicting the timing and scale of the next rate cycle. Instead, ensure that your strategy prepares for several interest rate scenarios. The following are a few scenarios for consideration:

Scenario No. 1 – The Next Tightening Cycle

The Fed hikes rates multiple times in 2022 and begins to reduce the balance sheet. If this goes on without any material market disruption, the next rate cycle will be underway.

What to expect:

Institutions could see liquidity begin to decrease, loan demand increase, margins improve, and the economy move forward in a growth cycle.

Scenario No. 2 – The Fed Tests the Market

The Fed’s first rate hike following the Great Recession came in December 2015, and they didn’t hike rates again until December 2016.

This “hike and wait” strategy was emblematic of one of the longest economic recoveries in modern history. The Fed could find themselves in a similar strategy should the COVID Omicron variant (or others) create economic challenges such as persistent labor supply constraints, disinflation and/or geo-political risks.

What to expect:

Institutions would experience high liquidity, low-to-moderate loan demand and tight margins as the recovery takes longer than expected.

Scenario No. 3 – The Double-Dip Recession

We could enter a second recession that could be exacerbated by the Fed acting too soon and failing to identify unsustainable asset bubbles. This economic recovery doesn’t fit the mold of prior recovery cycles, so we’re in uncharted territory.

Stocks have done surprisingly well, reaching new highs each quarter since March 2020. There’s been plenty of talk about an unsustainable housing market as well. Any major asset bubble could trigger another recession, which would force the Fed to crank back up its accommodative policy tools. There are also concerns of the recent flattening yield curve ahead of potential rate hikes.

What to expect:

It’s Groundhog Day with even more liquidity, low loan demand, further margin compression and interest rates moving back to record-lows.

“History doesn’t repeat itself, but it often rhymes.” This famous quote by Samuel Clemens (aka Mark Twain) is especially fitting today. The challenges brought on by the COVID-19 pandemic have been unprecedented, so answering the question of “what’s next” is no easy task.

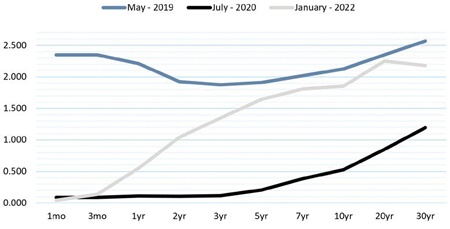

However, recent history can at least provide a framework for strategy development. For example, we know that in every case where the United States Treasury yield curve has inverted, an economic recession was soon to follow.

Strangely enough, months before the very first case of COVID-19, the yield curve inverted in May 2019 (Exhibit 2). It’s entirely plausible that even if the pandemic hadn’t unfolded, a (less severe) economic downturn may have been inevitable.

Most financial institutions are asset sensitive and perform better in a rising rate environment. Generally, margins increase in rising rate environments, but that depends on the shape of the yield curve.

Bond yields have recently moved in a bear flattener position where interest rates have moved higher, but the difference between short- and long-term yields have compressed. In fact, 2022 began with an inverted yield curve as the 20-year treasury traded slightly higher than the 30-year long bond.

January’s yield curve is also the flattest it’s been ahead of a potential Fed tightening cycle (Exhibit 2). That’s not exactly an ideal recipe for margin improvement.

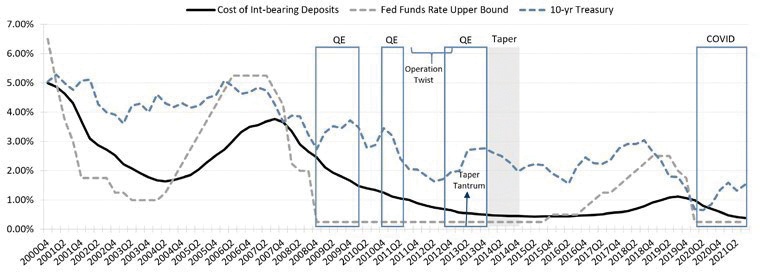

The chart in Exhibit 3 shows the changes in the upper bound target for the Fed Funds Rate and 10-year Treasury relative to the cost of interest-bearing deposits for members of FHLBank Topeka since 2000. The chart also highlights the Fed’s Quantitative Easing and Tapering activity.

One takeaway is that in both the rising rate periods that began in 2004 and 2015, respectively, deposit costs didn’t reach their peak until the Fed had already reversed course and began lowering interest rates. If this trend persists as the Fed potentially increases rates this year, it could be 2023 before we see the next peak in member deposit rates.

A second takeaway is the 10-year Treasury yield reaches a terminal high ahead of the peak in Fed Funds. This pricing behavior can serve as a better forward-looking indicator in the market. Unlike the prior two rising rate periods, the 10-year is well ahead of the Fed.

There’s a lot to unpack here with more questions than answers for members. But now, more than ever, thoughtful preparation for multiple rate path scenarios can go a long way to mitigate these uncertainties.

As always, the FHLBank Topeka team is here to help our members achieve their performance objectives and will continue to be a resource as we move forward in 2022.

Drew Simmons is the Oklahoma Regional Account Manager for FHLBank Topeka. He has more than 20 years of experience in the industry. Drew studied finance at Oklahoma City University. He can be reached at 800.933.2988 or at drew.simmons@fhlbtopeka.com.