We are ready for a challenging legislative year in 2026. 2025 proved to be a year of fast-paced change, especially on the federal front.

Federally, here is what we are working on.

Sens. Josh Hawley (R-MO) and Bernie Sanders (I-VT) are sponsors of a 10 Percent Credit Card Interest Rate Cap Act, which would impose an all-in annual percentage rate cap of 10% on credit cards. The bill has not had a markup hearing yet. While the bill isn’t a current threat, the bipartisan sponsorship is a concern. We are ensuring lawmakers understand that interest rate caps restrict credit to those who may need credit the most.

The Trump administration has formally determined the Consumer Financial Protection Bureau’s (CFPB) current funding mechanism is unlawful, a move that puts the agency on track to close in the coming months when its existing cash runs out. On Nov. 11, the DOJ notified federal courts that the CFPB anticipates exhausting available funds in early 2026, based on an Office of Legal Counsel opinion concluding that there are no “combined earnings of the Federal Reserve System” from which to transfer under 12 U.S.C. § 5497 while the Fed operates at a loss. The DOJ indicated that the Bureau expects to continue normal operations at least through Dec. 31, 2025, but a lapse would trigger Antideficiency Act constraints — pausing most rulemaking, examinations and enforcement except for narrow “emergency” functions. If a funding lapse occurs, rulemakings like Section 1071 could slow or pause, timelines could slip, and federal oversight gaps might spur more state attorney general and regulator activity.

Sen. Hagerty’s Deposit Insurance Reform bill had a House hearing. The proposal would increase coverage on non-interest-bearing business accounts to $10 million. The GSIBs are exempt, and smaller banks would not pay for the increase. Banks over $10 billion would pay. Many have stated that there is not any immediate cost expected. The FDIC has given a response to several questions asked by members of Congress, but the FDIC’s response is confidential.

After the House hearing, it is clear the bill will not pass in its current form. CBA has joined several other states in lobbying for changes to the Transaction Account Guarantee (TAG) program, making the TAG ability permanently in place and not requiring Congressional action to activate TAG.

While we continue to push for broad DIF reform, the window of time is very narrow to get anything. To date, no one is opposed to the TAG proposal, which may be all we are able to get.

The GENIUS Act/Stablecoin was signed into law on July 18. We continue to be concerned about the potential for funds to leave the banking system and be deposited in stablecoins. If that were to happen, the impact on access to credit would be damaging to the economy.

Permitted issuers must maintain reserves backing the stablecoin on a one-to-one basis using U.S. currency or other similarly liquid assets. Bank deposits are not insured one-to-one. This may increase the desirability of stablecoins.

The bill states stablecoin issuers are explicitly prohibited from paying interest or yield to holders of their stablecoins. This prohibition does not apply to affiliates. We are working to close this loophole through a market structure bill.

These are the changes we are asking for:

- Strengthen the prohibition on interest payments for payment stablecoins by extending it to brokers, dealers, exchanges and affiliates of payment stablecoin issuers.

- State Chartered Depositories: Repeal Section 16(d) of the GENIUS Act to restore state authority over out-of-state chartered financial institutions. Many are acting as money transmitters.

- Nonfinancial Company Activity: Close loopholes in the prohibition on nonfinancial companies being payment stablecoin issuers by removing all approval pathways and prohibiting both public and private nonfinancial entities.

Bills have been introduced to increase regulatory asset thresholds and index them for inflationary growth. There is a proposal that increases the current Dodd Frank Act (DFA) $10 billion threshold to $50 billion. The concern is that the Senate doesn’t have the appetite to take the threshold that high. Congress is trying to find what increase would pass. It is important to note that this threshold increase would not apply to the Durban amendment. We have lobbied for it to be included, but the inclusion of Durbin would most likely kill the bill.

The Supervisory Modifications for Appropriate Risk-Based Testing Act of 2025 would increase the threshold for a limited-scope examination after an on-site, full-scope exam from $3 billion to $6 billion.

The Tailored Regulatory Updates for Supervisory Testing Act of 2025 would increase the total asset threshold under which institutions qualify for an 18-month exam cycle from $3 billion to $6 billion.

We will continue to seek opportunities to increase and index all regulatory thresholds.

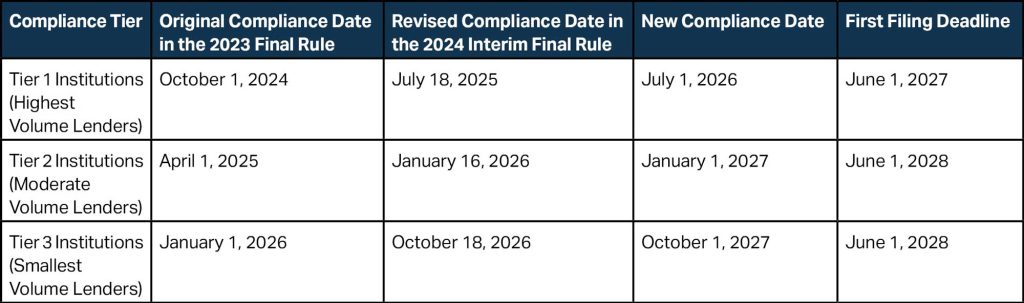

CFPB has proposed new rules regarding 1071 and 1033. We are also lobbying Congress to make permanent changes to prevent the yo-yo effect with the next administration. At the time of drafting this article, we did not yet have the proposed changes to the 1033 rules. These are 1071 proposed changes (November 2025):

- Narrowed Scope: Exclude some agricultural lending, merchant cash advances and loans under $1,000 (inflation-adjusted).

- Higher Thresholds: Increase the number of covered credit transactions needed to qualify as a “covered financial institution.” Increasing the threshold from 100 to 1,000 originations in each of the two preceding calendar years, using only small business originations (not small farm).

- Set a single compliance date — Jan. 1, 2028 — for institutions above the threshold in both 2026 and 2027. Institutions can begin collecting limited demographic data 12 months before their compliance date to test systems.

- Tighten the “small business” definition from gross annual revenue of $5 million or less to $1 million or less, with future inflation adjustments in $100,000 increments every five years starting in 2035. The Bureau is seeking SBA approval for the alternative size standard and highlights alignment with Regulation B and the CRA “smaller business” revenue metric.

- Confine initial data to statutory fields and a small set of discretionary items needed to make those statutory fields useful (e.g., NAICS code, time in business, number of principal owners). The CFPB proposes to remove several discretionary fields, including application method, application recipient, denial reasons, pricing components (including interest rate and fees) and number of workers.

- Change the demographic collection in two ways. First, consistent with Executive Order 14168, the proposed rule would remove LGBTQI+ owned business status and require the collection of principal owners’ sex using a static male/female choice. Second, while the rule would still require race/ethnicity for principal owners, the Bureau seeks comment on whether to move from disaggregated subcategories to only aggregate categories in the initial build to reduce complexity. The right for applicants to refuse to provide demographic information would be more prominent.

The compliance effective dates have also been changed.

The state legislature will provide plenty of sleepless nights, too, as the session began Jan. 14, 2026.

Artificial intelligence continues to be a concern for banking and the broader business community. At this point, we don’t anticipate one bill from the governor’s task force. But CBA worked collaboratively with consumer groups ahead of the special session and agreed on the language. Moving forward with AI, we anticipate that the compromise language would still be honored. Sen. Rodriquez has made a commitment to CBA to honor the language:

- Clarifies that the bill applies to consumers only;

- Limits consequential decisions to opening and closing of accounts/loans, setting of payment schedules and interest rates, and denial of credit;

- Exempts AI used for fraud prevention;

- Exempts many daily transactions; and

- Permits notification on a monthly statement.

Interchange had so much uncertainty as we are working diligently to thwart a bill to be reintroduced in Colorado. We know there are legislators who would like to introduce a pared-down interchange bill, no interchange on taxes for a portion of the business industry. They fail to realize that it would still take a complete overhaul of the system for one state. No interchange legislation has been passed in any state in the U.S. The Illinois litigation is not resolved, and any legislation in Colorado is 100% likely to result in litigation and high litigation costs to the state.

Credit unions continue to want to be banks without paying their fair share of taxes or regulatory compliance. We are expecting a bill that would permit credit unions to accept public deposits in 2026 or 2027. We face that legislative fight every few years. We are not expecting a bill to permit credit unions to buy a bank in 2026 or 2027 as well — we have defeated that bill the previous two years.

We are working with AARP on an Elder Abuse bill. This would be an expansion of the bill that passed several years ago. AARP has provided CBA draft language and is working collaboratively with us. The bill aims to give financial institutions greater legal flexibility to hold funds when they suspect fraud. We are working on language that protects banks from failing to stop a transaction and for holding funds, whether a transaction is proven to be fraudulent or not. We also want to ensure that any information banks are required to give under the state law does not violate any federal privacy regulations.

The Estate Non-Profit bill will be sponsored by Sen. Coleman, the Senate president. This bill is brought by the Nonprofit Association to address a gap in probate proceedings. An individual may bequeath their fiduciary account, bank account, investment account or IRA, for example, to a non-profit group. Some financial organizations have taken an extended period of time once the estate is settled to transfer the funds to the said non-profit. The proposed bill will place guidelines on the disbursement of funds once the estate is settled to the non-profit. CBA is working closely with the Nonprofit Association to ensure FDIC-insured institutions are protected, and reasonable guidelines are placed in the bill.

We know there will be a few surprises during the session, but we stand ready to defend the industry.

Don’t hesitate to reach out to either of us.

Jenifer Waller

jenifer@coloradobankers.org

Alison Morgan

alison@coloradobankers.org