Throughout the course of the pandemic, households have accumulated significant savings. Banks, awash in deposits and with interest rates still at low levels, have increased lending while working through the many challenges of the past year, including maintaining services to existing customers. Despite the operational obstacles brought on by the pandemic, most financial institutions have managed to attract new customers, which has further aided the growth in asset size for institutions nationwide. The Paycheck Protection Program (PPP) has also contributed substantially to this growth.

While the economy gradually adjusts from heavy government stimulus and returns to growth levels seen before the pandemic, banks are adapting to new ways of serving their customers. Beyond the logistical challenges of in-person meetings and modifications to branch operations to maintain service quality to customers, banks have mostly resorted to bolstering the use of Digital Channels to continue to operate and thrive throughout the pandemic.

The rapid adoption of Digital Banking has exacerbated the need for banks to have responsive and innovative digital and mobile offerings. Indeed, the pandemic accelerated the use of such channels among a rising set of customers who may not have interacted with their financial institution in this manner before. For banks that are really tuned into their customer base, it is obvious that effective digital channels must be a part of current and future strategy. This is the contemporary path to service quality for those banks, and they are prepared to invest in it.

Notably, service quality is mostly the result of the management and philosophy of the bank. As with most any business, customers want to see that their bank cares — that it values the relationship and understands the customers’ needs regardless of where and when the interaction takes place. If banks embrace this intense customer focus, they will forge new paths to service quality. One ICI Consulting client that kept its branches open and operational boldly stated, “We never had to ask our customers to make an appointment to visit a branch.”

In part, service will only be as good as the software tools banks use to implement Digital Banking. Therefore, a comprehensive survey of the institution’s requirements, and a rigorous evaluation of current offerings, are demanding the attention of bank executives to be competitive in the market, responsive to existing customers, and in a position to attract new ones. Banks must look ahead to a time when the economy stabilizes, employment returns to normal levels, and people embrace their everyday routines. To secure a long-term and stable customer base, banks will need to grow by catering to a younger demographic while still providing superior service to their clients. Attracting and servicing future generations will require innovative new products and services delivered through Digital Channels. Banks must also anticipate the likely challenges ahead and be prepared for a time when growth levels out. When this occurs, one of the most dependable actions is to control costs.

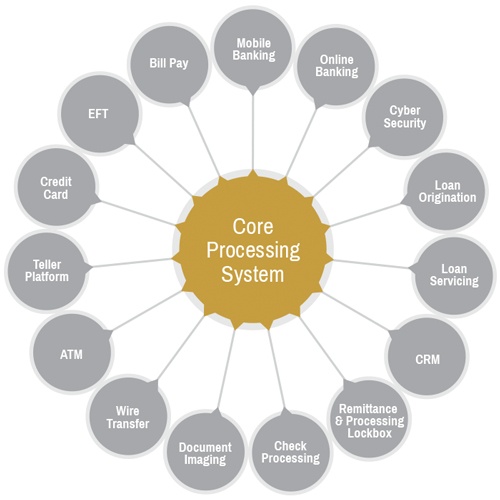

With few exceptions, Data Processing expenses are among the top three expenditures, along with Salary & Benefits and Premises & Fixed Assets that a financial institution incurs on an ongoing basis. Data Processing expenses, which include an institution’s spending on Core Processing & Ancillary Systems, are easily addressable cost reduction targets.

The Ancillary Systems are key applications that surround and interact with the Core System. They include important services like ATM/EFT, Credit Card, Online Banking, Mobile Banking, Loan Origination & Servicing, Payments, Wire Transfer, Cash Management, Document Management, BSA/AML, IT Security, Check Processing, among others. These Ancillary Systems are as important as the Core System because they not only support the key business functions of the institution, but also serve as touchpoints for customers.

We also see banks aggressively pursuing new strategies to expand and emphasize Digital Channels — many that shrewdly started such projects prior to the onset of the pandemic. In modernizing their Digital Channels, banks are not only reaching more customers, but they are also doing so with more innovative and integrated applications while potentially reducing data processing spend. Furthermore, they are making a sound investment in what will become a vital channel through which customers will be served in the future.

Banks are also making changes to the Digital Channel to address a shifting mix of commercial or consumer business, integration to the Core System, and even because of variable vendor product and support plans. When reviewing Data Processing systems contracts, ancillary grouping products that serve the Digital Channel with other important applications and especially the Core System will naturally increase the purchasing power and thus negotiation leverage for the bank. We commonly recommend this holistic approach to our clients as it tends to yield the best results.

The rapid adoption of Digital Banking has exacerbated the need for banks to have responsive and innovative digital and mobile offerings.

Banks will do a great service to their customers and shareholders by closely examining and monitoring Data Processing costs. There is a wide range of pricing models in the industry. The best way to gain insight into comparable market prices is to conduct a competitive evaluation of alternatives. The banks that take the time to do so and start the process 24 to 30 months prior to contract expiration will see the best outcome. In terms of finding solutions that effectively serve customers and addressing the institution’s business requirements at the best price and terms.

This goal can be mainly achieved by either negotiating new technology contracts or renegotiating existing technology contracts. While some executives deem the technology review process painful, it nevertheless remains an important part of appropriate due diligence by the institution in a key area that is the foundation of efficient and cost-effective operations. Unless the bank enjoys annual contracts, most banks maintain multi-year contracts with the vendors of Core Processing and Ancillary Systems. With the opportunity to review alternative solutions and/or address costs only every five, seven or 10 years, it is wise to take advantage of the typical contract cycle to carefully review these business-critical applications. If not then, when?

Since 1994, ICI Consulting has been a leading bank and credit union advisor nationwide. ICI is a consulting firm that supports financial institutions by providing core processing assessments, gap analyses, vendor evaluations, contract negotiation and conversion services. ICI Consulting is well known for saving clients time and money during core processing & ancillary systems evaluations and negotiations with the providers of these business-critical solutions.Learn more at ici-consulting.com.